WASHINGTON, D.C., 10/26/2021 – Wine & Spirits Wholesalers of America’s (WSWA’s) SipSource released today the latest set of CSI (Channel Shifting Index) data that provides wine and spirits professionals access to channel performance data for wine and spirits categories/segments, price tiers, and U.S. regions that are easy to understand and relevant to navigate the challenges COVID is continuously throwing at the industry.

WSWA’s SipSource is the most comprehensive source for channel performance and shifts—based on distributor depletion data across both off- and on-premise channels and sub-channels, at a national and U.S. Census division level.

The Latest SipSource CSI Tells Us:

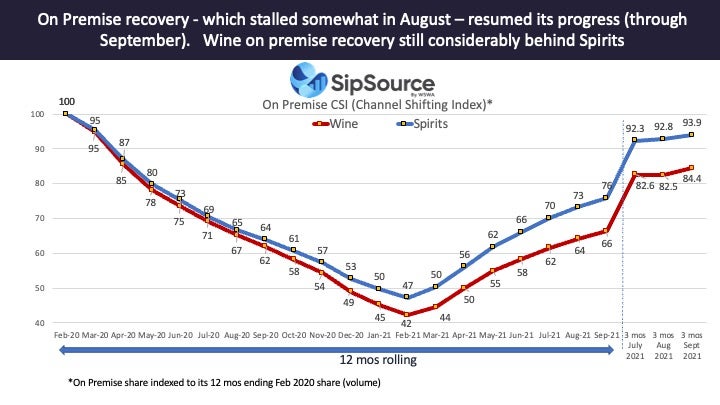

“The on-premise CSI which was steadily improving through July, but stalled in August, advanced again in September,” said Danny Brager, SipSource analyst and industry veteran. “This advancement substantiates the channel’s longer-term recovery from COVID-related impacts. The combined wine and spirits CSI for on-premise reached a high of 91 for the last three months – a 1.5 point improvement from the prior three month period. That’s in comparison to the low of 45 in the twelve-months, ending February 2021,” Brager added.

The most recent CSI data quantifies the significant difference of the rate of recovery for on-premise for wine verses spirits. The September data shows spirits are performing much healthier (index of 94) on-premise than wine (index of just over 84).

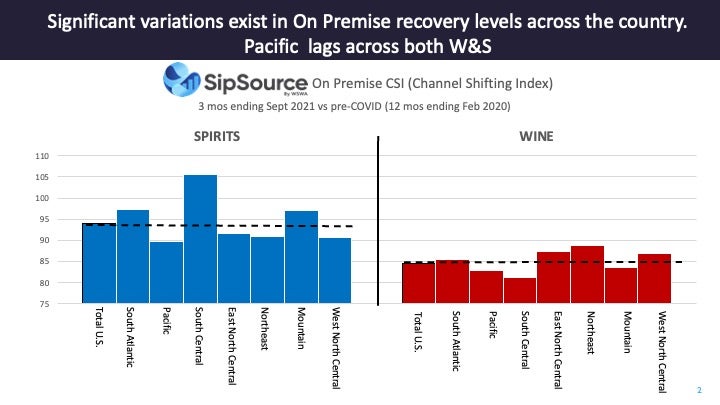

When looking at the CSI data, regional discrepancies also continue to be visible. The SipSource on-premise CSI for both wine and spirits was the lowest in the Pacific region (with California as the largest state). On the positive side, in the South Central, where Texas is the largest state, spirits on-premise CSI is greater than 100 – indicating a full recovery when compared to pre-COVID dates. Likewise, the South Atlantic and Mountain division areas are both approaching 100.

While wine’s on-premise CSI remains under 100 everywhere, it did improve significantly in both the Northeast and West North Central parts of the U.S.

“When we go deeper into on-premise channels, the Recreation channel has bounced back the fastest over the longer term,” added Brager. “On the flip side, the Lodging and Transportation channels remain well behind where they were pre-COVID, indicating the travel-related business continues to suffer the impact the pandemic.”

The September SipSource on-premise CSI revealed some product segments continue to advance, most notably:

- The on-premise CSI for Ready-to-Drink cocktails (RTDs) is now well over 200 for the past three months, indicating that the on-premise share of this segment, compared to its total business, has now more than doubled since pre-COVID. The growth reinforces the growing popularity of pre-mixed cocktails and RTDs.

- Cordials, Rum, and Brandy categories all have an on-premise CSI exceeding 100.

- Within the Wine segment, Champagne (with an on-premise CSI of 108 for the past three months) continues to be an important element of the overall, very positive story for sparkling wine generally. This segment is well above table wine’s on-premise CSI of just 81.

How to Read WSWA’s SipSource CSI Index:

The SipSource CSI provides monthly comparisons of channel importance to pre-COVID levels (12 months to February 2020). An index above 100 indicates the channel referenced has a greater share of the market than it had pre-COVID; an index less than 100 indicates that the channel has a smaller share of the market than it had pre-COVID. In particular, on-premise business was devastated during the height of the pandemic and is now in various stages of recovery. But wine and spirits are not recovering equally—nor are the segments within each category, the regions within the country, or the various trade sub-channels.

This data will enable you and your teams to answer the unknowns such as:

- Where should you focus/invest? Where should you hold back?

- Are you keeping pace with overall category/segment trends in various channels?

For members of the media who wish to discuss CSI data with a SipSource analyst, please contact Michael@WSWA.org.

For professionals interested in subscribing to this data set, please contact Nicole@wswa.org.

About SipSource by WSWA

Wine & Spirits Wholesalers of America’s (WSWA’s) SipSource is the ONLY source for aggregated distributor depletion data, built from unique items sold to individual stores. Since wholesalers distribute to all types of retailers, SipSource has unrivaled channel segmentation. It also covers the largest volume of bona fide alcohol sales and does not need to rely on estimates, samples or projections. WSWA’s SipSource uses an industry leading platform: VIP’s iDIG to deliver timely, transparent and trusted data. In addition to the reporting tool, subscribers have access to quarterly and annual reports that leverage powerful collaboration with industry leaders and provide high-level insights into the wine and spirits marketplace.

Interested in subscribing to SipSource? Please contact Nicole Anderson at nicole@wswa.org for more information.

###